Topic 3: HOW TO MAKE YOUR HOME LOAN INTEREST FREE

If you are planning to take a home loan or have an existing home loan, you would be paying interest to a bank or housing finance company. As

one repays the home loan through monthly EMIs, the accumulated interest cost over the tenure of the home loan can be astronomical.

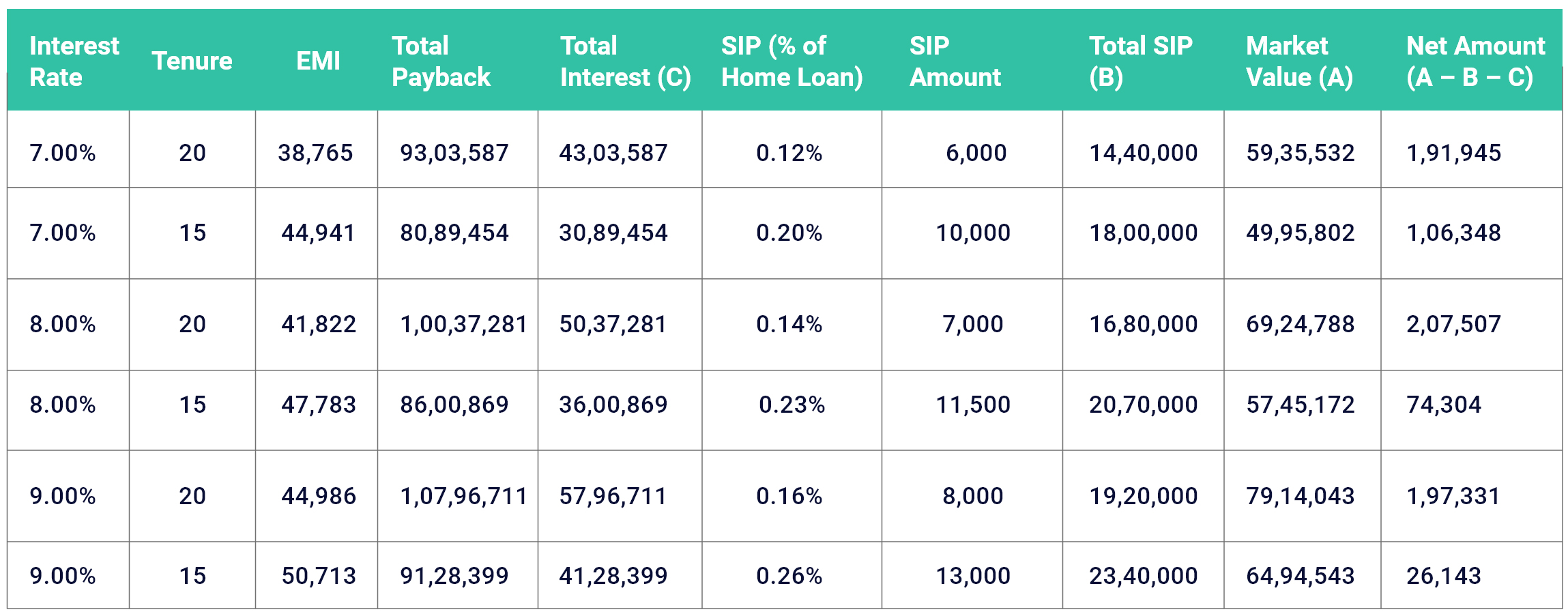

For example, a home loan of ₹50,00,000 for a period of 20-years at 7.0% interest has an EMI of ₹38,765 and would make one pay a total of ₹93,03,587 (₹ 50,00,000 principal & ₹43,03,587 interest cost).

However, there’s a simple trick that can help make this home loan interest-free. For a home loan of 15-20 years, by starting a SIP of 0.10-0.25% of your total home loan amount outstanding, you can recover your total interest cost.

The SIP amount would vary depending on the home loan interest rate, tenure, and market returns.

Illustration: For a Home loan of ₹50,00,000

Assumptions: Returns from investment: 12.0%

Net Amount: Market Value of SIP less Total Investment through SIP less Total Interest Cost

A positive net amount in the above table indicates that one can recover the entire interest cost and the capital invested through SIP with a disciplined investment approach.

Note: For higher interest rates and lower tenure, the percentage of total outstanding required for SIP would be higher.

For example, a home loan of ₹50,00,000 for a period of 20-years at 7.0% interest has an EMI of ₹38,765 and would make one pay a total of ₹93,03,587 (₹ 50,00,000 principal & ₹43,03,587 interest cost).

However, there’s a simple trick that can help make this home loan interest-free. For a home loan of 15-20 years, by starting a SIP of 0.10-0.25% of your total home loan amount outstanding, you can recover your total interest cost.

The SIP amount would vary depending on the home loan interest rate, tenure, and market returns.

Illustration: For a Home loan of ₹50,00,000

Assumptions: Returns from investment: 12.0%

Net Amount: Market Value of SIP less Total Investment through SIP less Total Interest Cost

A positive net amount in the above table indicates that one can recover the entire interest cost and the capital invested through SIP with a disciplined investment approach.

Note: For higher interest rates and lower tenure, the percentage of total outstanding required for SIP would be higher.