Topic 1: CURRENT MARKET AFFAIRS

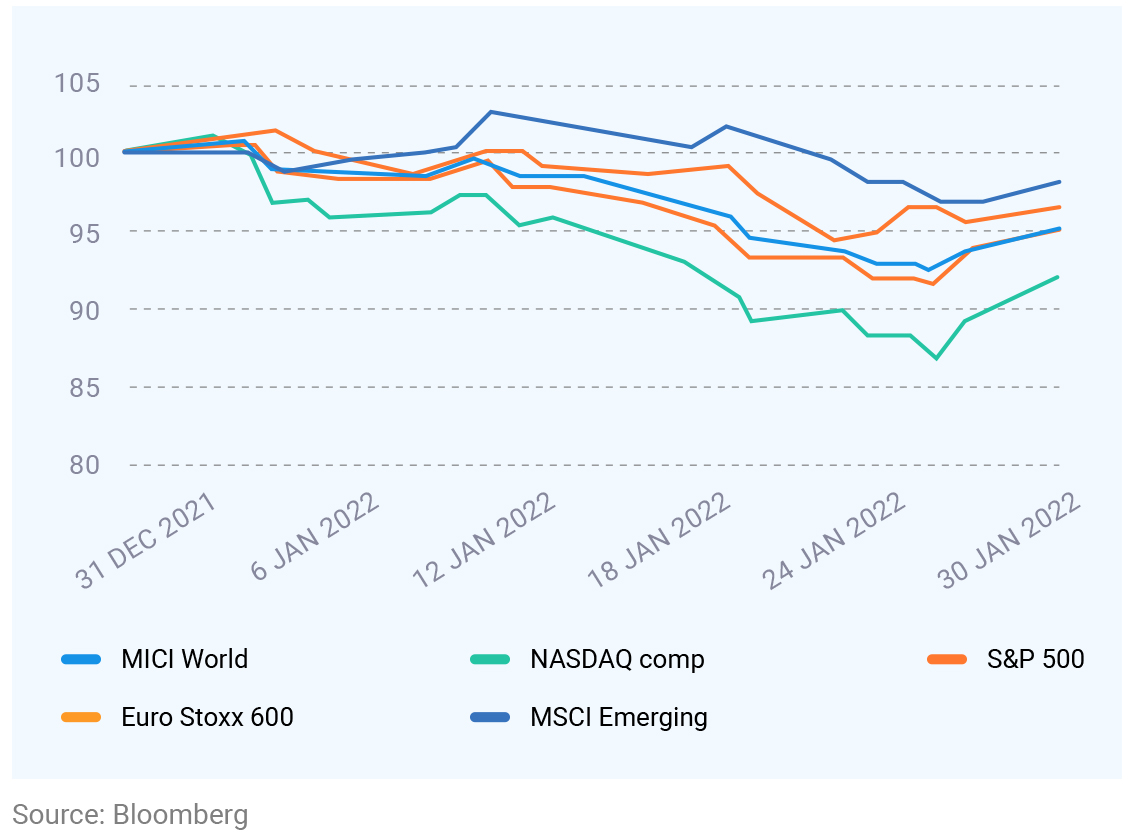

1. EQUITY MARKETS & THE END OF FREE MONEY

The world’s stock markets witnessed heightened volatility in the first

month of 2022 as investors prepared for tighter monetary policy. The

S&P 500 (proxy for the US market) and Nasdaq (a tech-heavy index)

suffered their worst monthly declines since March 2020, falling 5.3%

and 9.0%, respectively. It was also the S&P 500′s most significant

January decline since 2009. Markets elsewhere have also witnessed

similar volatility. Investors flocked out of growth-oriented technology

companies as higher interest rates would lower the value of the future

profits of these companies

EQUITY MARKET PERFORMANCE

The US Fed signaled that it would raise interest rates in March to bring

inflation under control. That will be the first increase since 2018. The

Fed also signaled that it would wind down its bond-buying program,

which expanded during the pandemic.

We believe that markets will soon learn to live with tightening monetary

policy and reward companies with strong earnings growth. To benefit

from the ongoing volatility, we continue to recommend allocating to

equity through the SIP route.

RUSSIA’S ROULETTE

Tensions between Russia and Ukraine are showing no signs of abating.

While we expect the deadlock shall be resolved through diplomacy, we

are watching for the impact on asset prices if the conflict escalates.

Energy and commodity markets could see an immediate effect if the

situation worsens. Also, the ripple effects could be more broad-based

and impact global inflation expectations and monetary policy.

When the world is dealing with rising energy prices and supply-demand

imbalances in several metals and commodity markets, a steady supply

of commodities from Russia is crucial. Russia is one of the world’s

largest exporters of critical metals. Any disruption to these exports

could amplify global inflation.

History tells us that geopolitical issues are simmering all the time, and

such conflicts do not have a lasting impact on the markets. If a

resolution is achieved, the markets will react positively. Even in the case

of a stalemate, the markets might shrug off fears of a worse outcome.

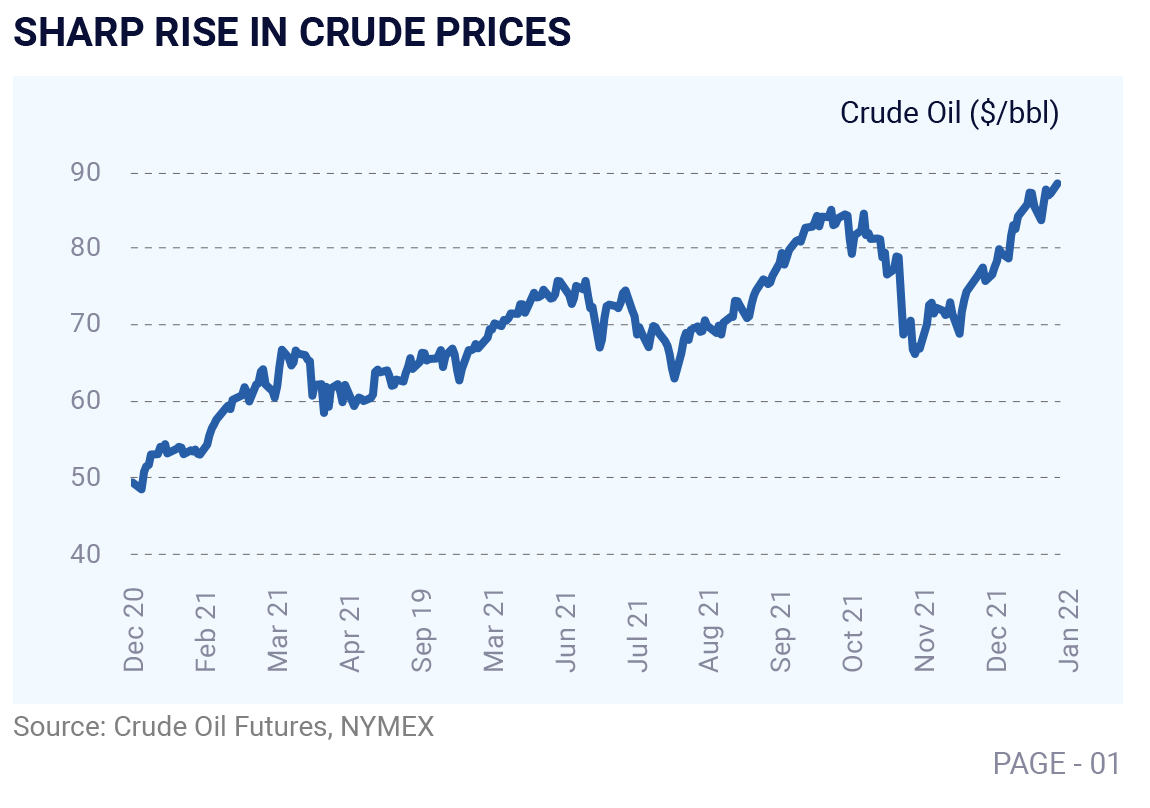

THE SURGE IN OIL PRICES

The rally in the crude prices shows no signs of slowing down as

pressure emerges from both the demand and supply sides. The global

output has fallen short of consumption by an average of 1.4 million

barrels per day last year, bringing the cumulative inventories to the

lowest level in 7-years. As economies emerge from covid-19, we expect

demand for crude oil to remain elevated. Also, given the series of

supply outages, it has put $100 crude prices within reach