1. EQUITY MARKETS & THE END OF FREE MONEY

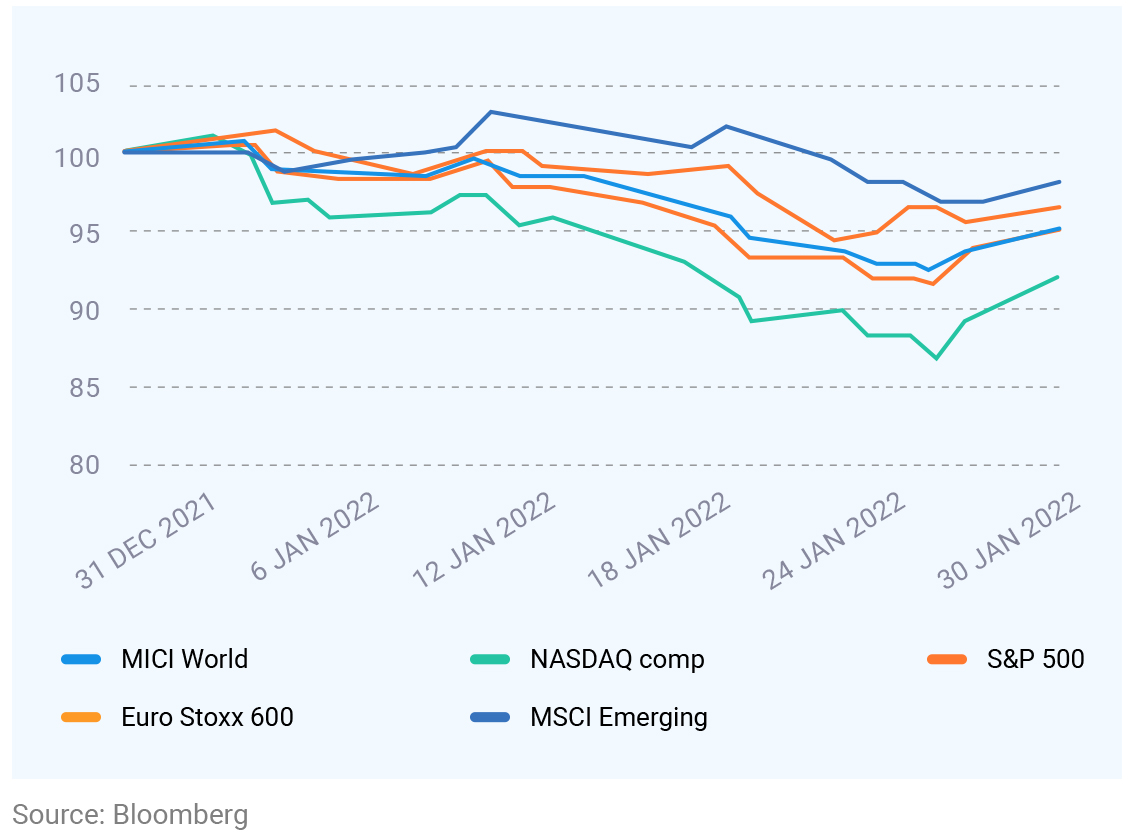

The world’s stock markets witnessed heightened volatility in the first

month of 2022 as investors prepared for tighter monetary policy. The

S&P 500 (proxy for the US market) and Nasdaq (a tech-heavy index)

suffered their worst monthly declines since March 2020, falling 5.3%

and 9.0%, respectively. It was also the S&P 500′s most significant

January decline since 2009. Markets elsewhere have also witnessed

similar volatility. Investors flocked out of growth-oriented technology

companies as higher interest rates would lower the value of the future

profits of these companies

EQUITY MARKET PERFORMANCE

The US Fed signaled that it would raise interest rates in March to bring

inflation under control. That will be the first increase since 2018. The

Fed also signaled that it would wind down its bond-buying program,

which expanded during the pandemic.

We believe that markets will soon learn to live with tightening monetary

policy and reward companies with strong earnings growth. To benefit

from the ongoing volatility, we continue to recommend allocating to

equity through the SIP route.

RUSSIA’S ROULETTE

Tensions between Russia and Ukraine are showing no signs of abating.

While we expect the deadlock shall be resolved through diplomacy, we

are watching for the impact on asset prices if the conflict escalates.

Energy and commodity markets could see an immediate effect if the

situation worsens. Also, the ripple effects could be more broad-based

and impact global inflation expectations and monetary policy.

When the world is dealing with rising energy prices and supply-demand

imbalances in several metals and commodity markets, a steady supply

of commodities from Russia is crucial. Russia is one of the world’s

largest exporters of critical metals. Any disruption to these exports

could amplify global inflation.

History tells us that geopolitical issues are simmering all the time, and

such conflicts do not have a lasting impact on the markets. If a

resolution is achieved, the markets will react positively. Even in the case

of a stalemate, the markets might shrug off fears of a worse outcome.

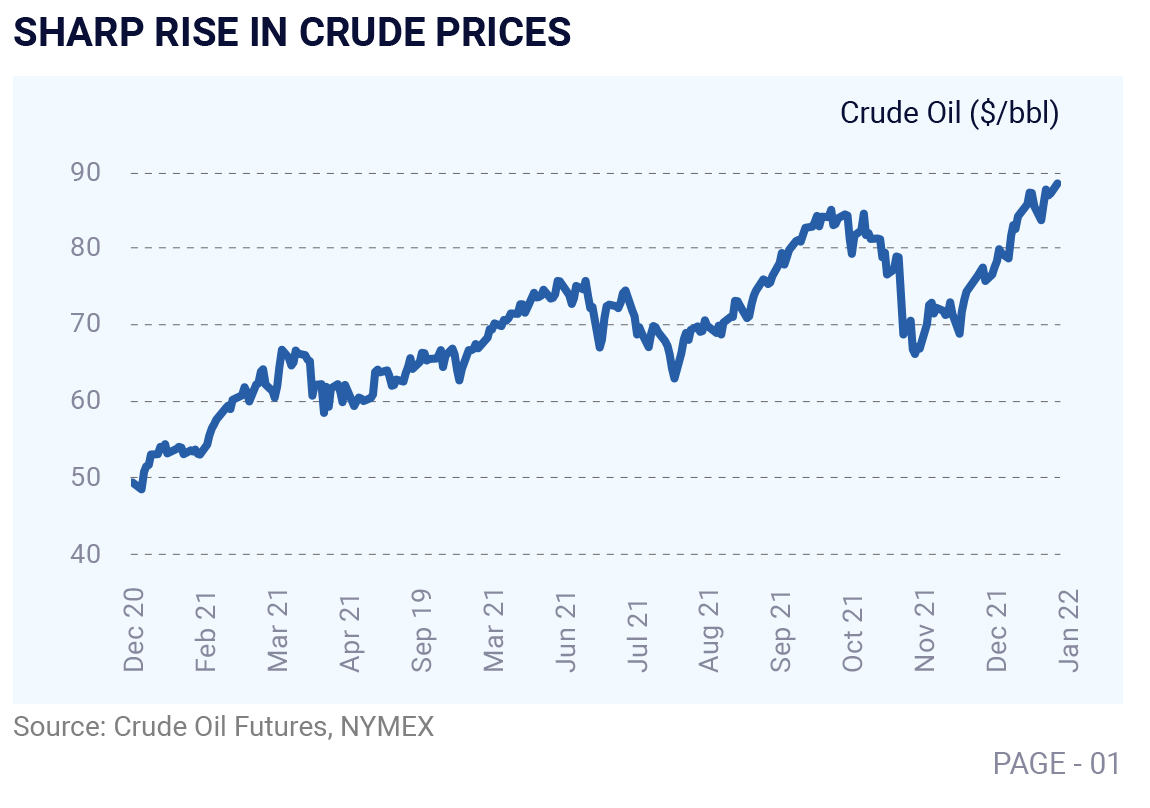

THE SURGE IN OIL PRICES

The rally in the crude prices shows no signs of slowing down as

pressure emerges from both the demand and supply sides. The global

output has fallen short of consumption by an average of 1.4 million

barrels per day last year, bringing the cumulative inventories to the

lowest level in 7-years. As economies emerge from covid-19, we expect

demand for crude oil to remain elevated. Also, given the series of

supply outages, it has put $100 crude prices within reach

Given the inflationary environment and central banks across the globe winding up ultra-loose monetary policies, the 10-year government security yields in India have increased by around 35-40 bps since the beginning of this year. The higher borrowing requirements of the center (as projected in the Union Budget) to fund the fiscal deficit, borrowing from the state governments, and revival in private credit shall put pressure on liquidity and bond yields. Such an increased supply of bonds in the market shall negatively impact the fixed income market.

As we expect interest rates to be volatile, it is best to avoid funds investing in long-dated securities. Thereby, investors can consider investing in securities with shorter maturity (short duration funds and banking & PSU funds). Also, one can consider investing in floater rate funds as returns are adjusted based on prevailing yields in the market. To benefit from the steepness of the yield curve, one can invest in funds with 2.5 to 4 years of duration and run a rolldown strategy.

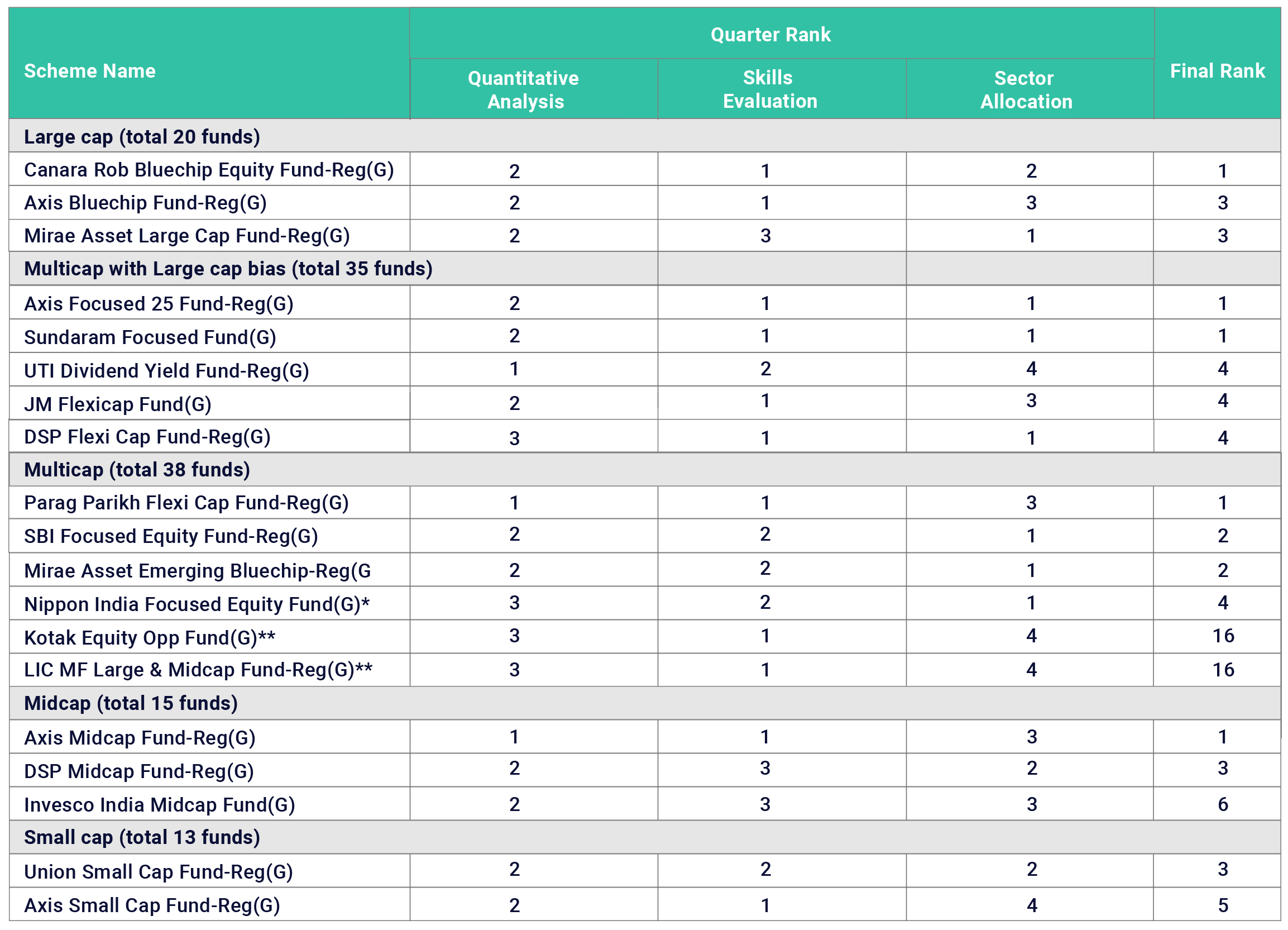

EQUITY OUTLOOK: THUMBS UP

The government’s growth and capital expenditure focus in the budget is positive for equity markets and has essentially put India back on its growth trajectory. This investment-led growth could provide a boost to jobs and incomes. We expect equity markets to perform well with long-term drivers in play and earnings for corporate India likely to rebound. In the near term, there are several headwinds such as US Fed tapering, geopolitical tension, and rising crude prices which could lead to increased volatility in the market. We believe that such market volatility should not concern investors with long-term investment horizons. Over time, this market volatility would be a minor blip (drawdown) in their overall returns. Also, investors with excess liquidity should use this market volatility as an opportunity to deploy funds.

The question then arises which are the right mutual funds to be considered for investing. We follow the analytical approach for recommending funds, focusing on three tenets viz. past performance, the manager’s ability to identify trends in the market, and their stock picking ability. We perform the entire process of fund selection every quarter to check for any deviation in our recommended funds.

The table below lists our recommended funds across different categories based on the December-end data.

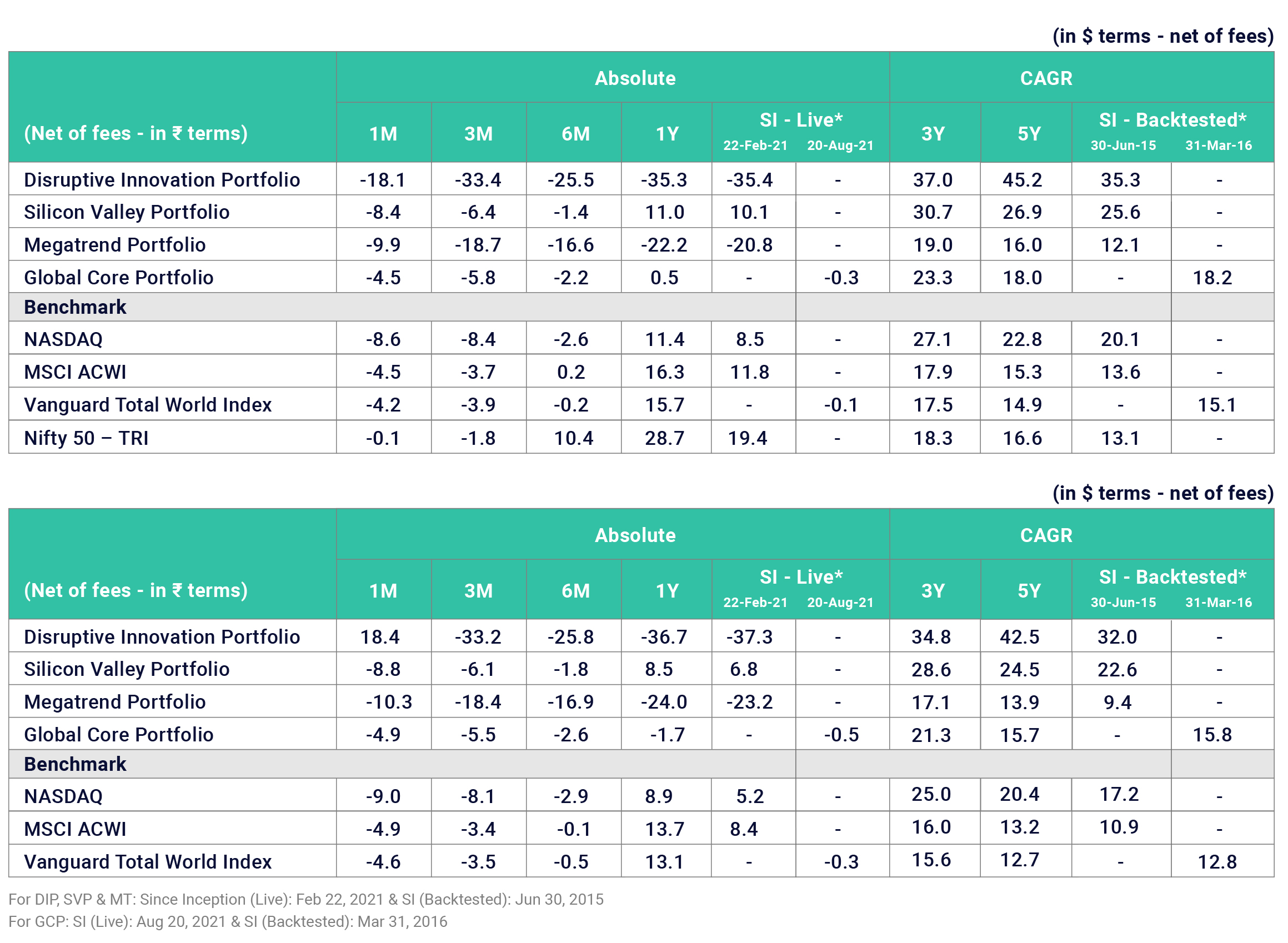

UPDATE ON GLOBAL INVESTMENT PORTFOLIOS

The Disruptive Innovation Portfolio (DIP) and the Megatrends Portfolio (MT) have investments in high growth/mid to smallcap tech stocks

exhibiting high revenue growth but little to no net income. This group of stocks did exceedingly well during the period Jan 2020-Third quarter

2021 for multiple reasons:

The US Fed responded very aggressively to the pandemic that caused massive economic disruptions. Not only had they cut the Fed Funds rate

to zero, but they were also aggressively printing money by actively purchasing bonds. At the same time, the government was aggressively

doling money out to individuals and corporations, much of which ended up in the stock market. The DIP and MT group of stocks were particular

beneficiaries of these fiscal and monetary actions:

- They were growing fast

- The discount to future earnings was small as inflation was nonexistent

- Many of them were considered big beneficiaries of Work From Home (WFH)

Since the last quarter of 2021, these trends have reversed dramatically, and these stocks have performed very poorly. The DIP and the iShares Russell 2000 Index (smallcap index) represent these trends (chart 1).