Russia’s invasion of Ukraine happened just when markets were getting

ready for a series of Fed rate hikes, and encouraging signs were emerging

that the world was finally moving to an endemic state of Covid.

Before this invasion, 2022 had already witnessed a selloff in global

equities due to high inflation numbers and central banks worldwide

pledged to end the easy liquidity situation. The Fed dot plot indicated

around seven rate raises of a quarter-point each this year, followed by a

few more rate hikes in 2023.

We were cautious on the markets even before the Russia-Ukraine crisis

unfolded. With several sanctions imposed on Russia, we expect further

disruption in the global supply chains, and this event will make inflation

worse. Even the euphoria in the consumer confidence that was finally

emerging from Covid after two long years may be curtailed by rising

geopolitical tensions.

India has played a balanced approach by not explicitly siding with any of

the major powers involved nor speaking up against them. However, the

surge in Oil & Gas prices due to global supply disruption poses a problem

for the Indian economy. Higher oil prices could cause a rise in retail

inflation and impact households’ discretionary spending. Also, it may

widen India’s current account deficit due to higher oil import bills. India’s

massive foreign exchange reserves shall help tackle any volatility in the

currency.

From an equity markets perspective, the ongoing conflict between Russia

and Ukraine could cause short-term volatility. The uncertainty around the

Uttar Pradesh state election results and the Fed’s meeting in mid-March

could impact the markets.

Given these headwinds, we would be cautious on the market and

recommend spreading your investments over the next 3-6 months. Most

stocks in the mid and smallcap segment have taken some beating due to

the recent volatility and are now available at cheaper valuations.

Systematically adding allocations to the midcap and smallcap segments

could benefit over 3-5 years.

Commodities, Particularly Oil & Gas As Well As Industrial Metals & Mining

This theme was already working well this year. The Russia-Ukraine event further bolsters the case for its continuing outperformance

Alternative Energy Companies

This theme was already working well this year. The Russia-Ukraine event further bolsters the case for its continuing outperformance

Defense And Aerospace

We posit that the invasion of Ukraine will lead to a big-spending ramp up in this sector, and significant global arms suppliers will be the

beneficiary

Global Shipping Companies

The disruption in supply chains and the need for Europe and Asia to increase their LNG shipments will keep shipping rates upward

Cybersecurity Companies

Cyberattacks are a big part of modern warfare among global powers. As Ukraine grinds on, the demand for companies that provide

Cybersecurity will surge rampantly

Banks And Other Lending Institutions

They are the beneficiaries of rising rate environment as the spread between their borrowing and lending rises

There are several products eligible for availing tax benefits under section 80C. These products range from life insurance policies to equity-linked saving

schemes (ELSS). Most investors consider investing in National Saving Certificate (NSC) or Public Provident Fund (PPF) as they are government-backed and

offer assured returns.

Any investment that offers assured returns and has low risk tends to offer moderate returns. On the other hand, investments in ELSS schemes can generate

higher returns at a higher level of risk. ELSS schemes are equity mutual funds, thereby can be volatile. These schemes invest across market capitalization

and have a lock-in period of 3-years.

The NSC, a post office savings product, is a fixed-income investment scheme offering an interest rate of 6.8% p.a. compounded annually with a lock-in of 5-

years. The PPF is also a fixed-income investment product offering an interest rate of 7.1% p.a. compounded annually with a lock-in of 15-years.

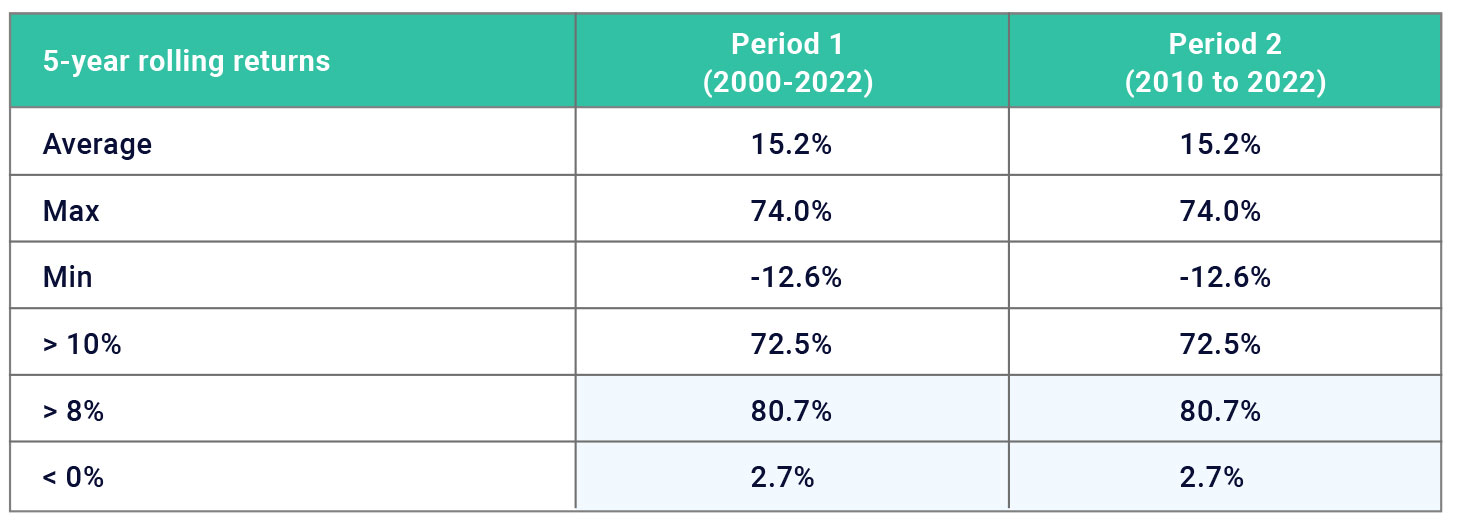

For an apple to apple comparison, we evaluate the rolling returns of 5-years, 7-years, and 15-years of ELSS schemes vis-à-vis returns offered by NSC and

PPF

For a holding period of any 5-years from 2000-2022 (month-end), the average performance of all ELSS funds stands at 15.2%. Over this period, almost

81% of the time, these ELSS funds have given returns more than 8%, beating the returns offered by both NSC & PPF. Also, only 2.7% of the time, these

ELSS funds gave negative returns for a 5-year holding period. Thereby, an investor with an even moderate risk appetite can consider investing in ELSS

funds over other secured investments given the potential upside these funds have to offer (average of 15.2% CAGR, and generated more than 10% returns

72.5% of the time).

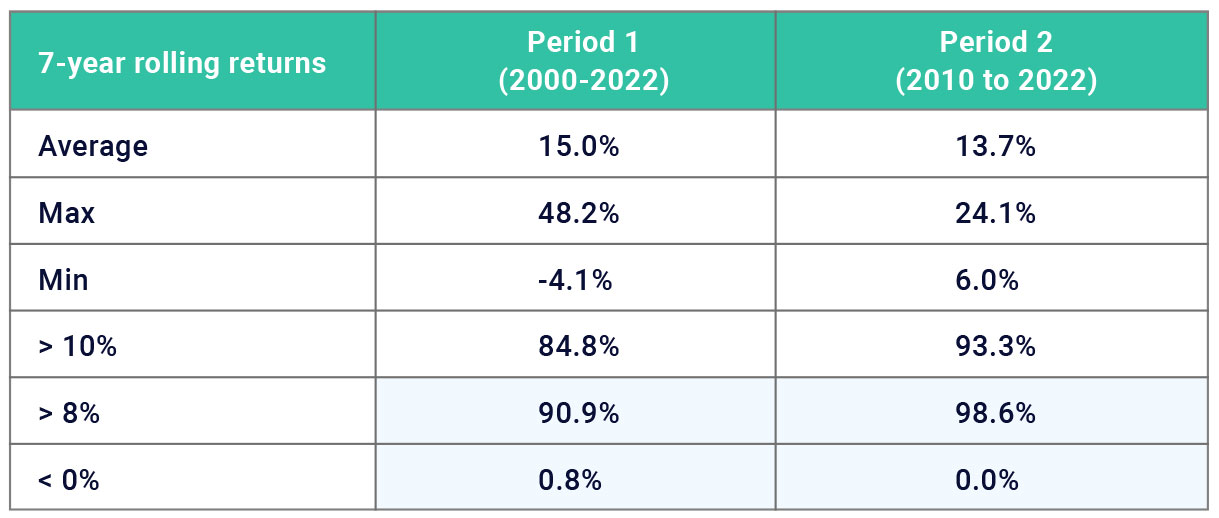

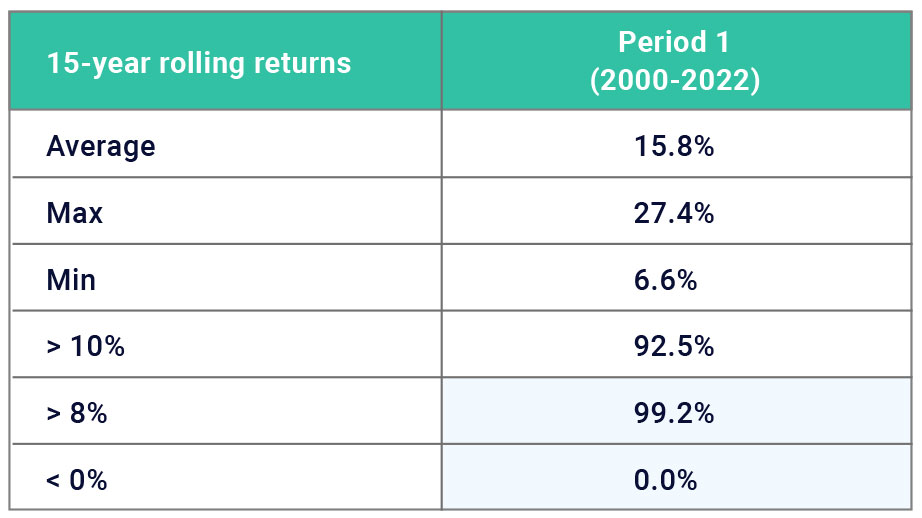

Similarly, when we look at a holding period of 7-years and 15-years, the case for investing in ELSS funds over NPS and PPF only becomes more robust

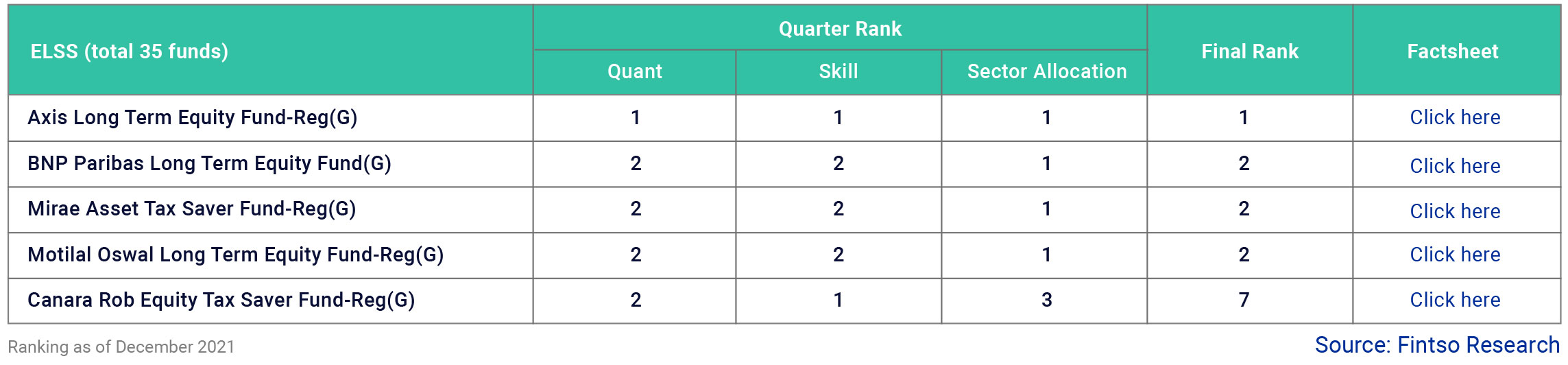

To further reduce the risk, we recommend investing in 2-3 ELSS schemes. Based on our fund selection process that considers performance and fund management aspects, below is the list of our recommended ELSS schemes.